Gold vs Silver: Key Differences for Investors

Gold is the steadier precious metal for investors who want a long-term store of value. Silver is its high-flying counterpart with sharper price swings tied to industrial demand.

Gold is the steadier precious metal for investors who want a long-term store of value. Silver is its high-flying counterpart with sharper price swings tied to industrial demand.

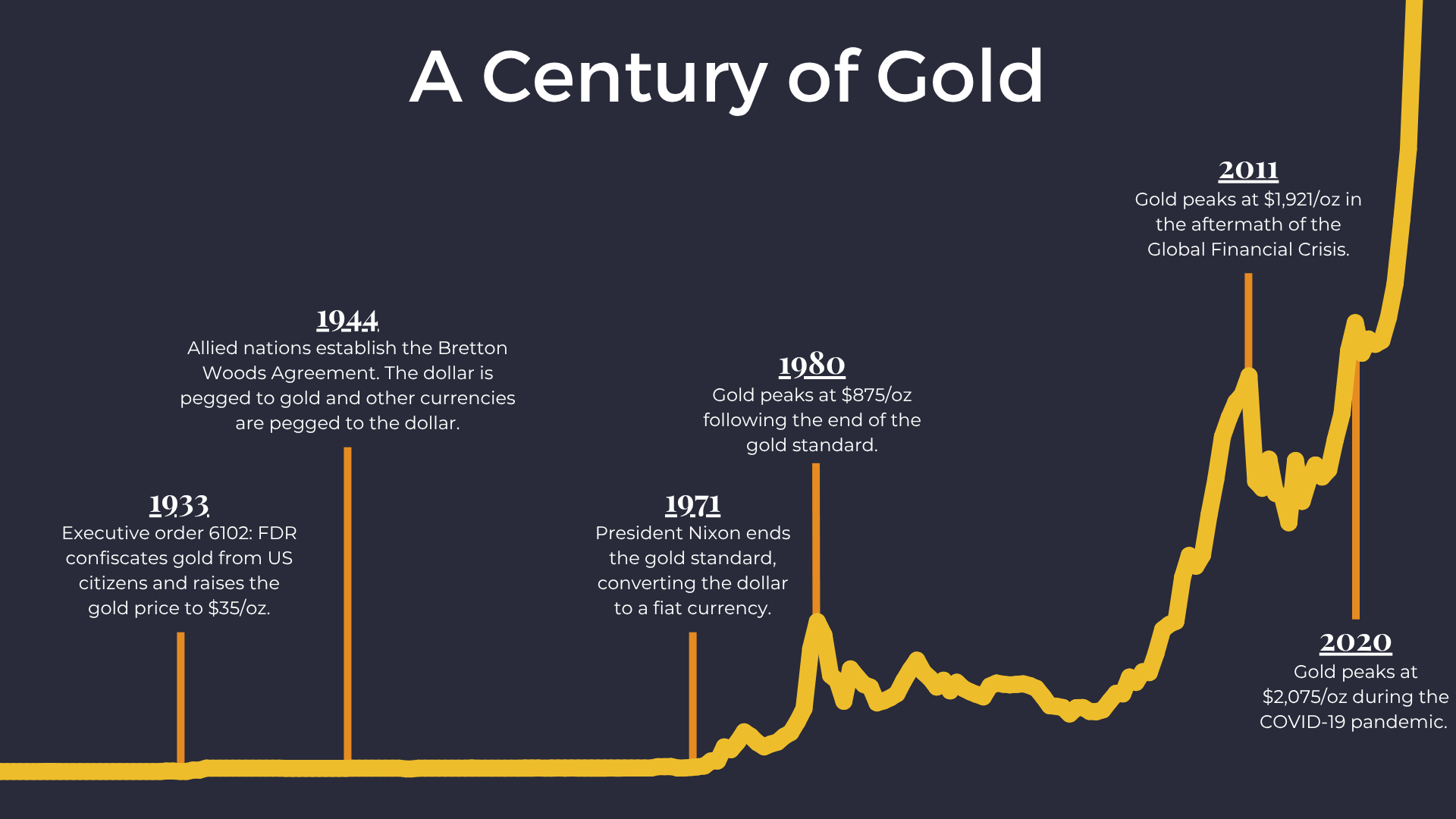

Could the U.S. government ever knock on your door and demand your gold like they did in 1933? We will take a look at the 1933...

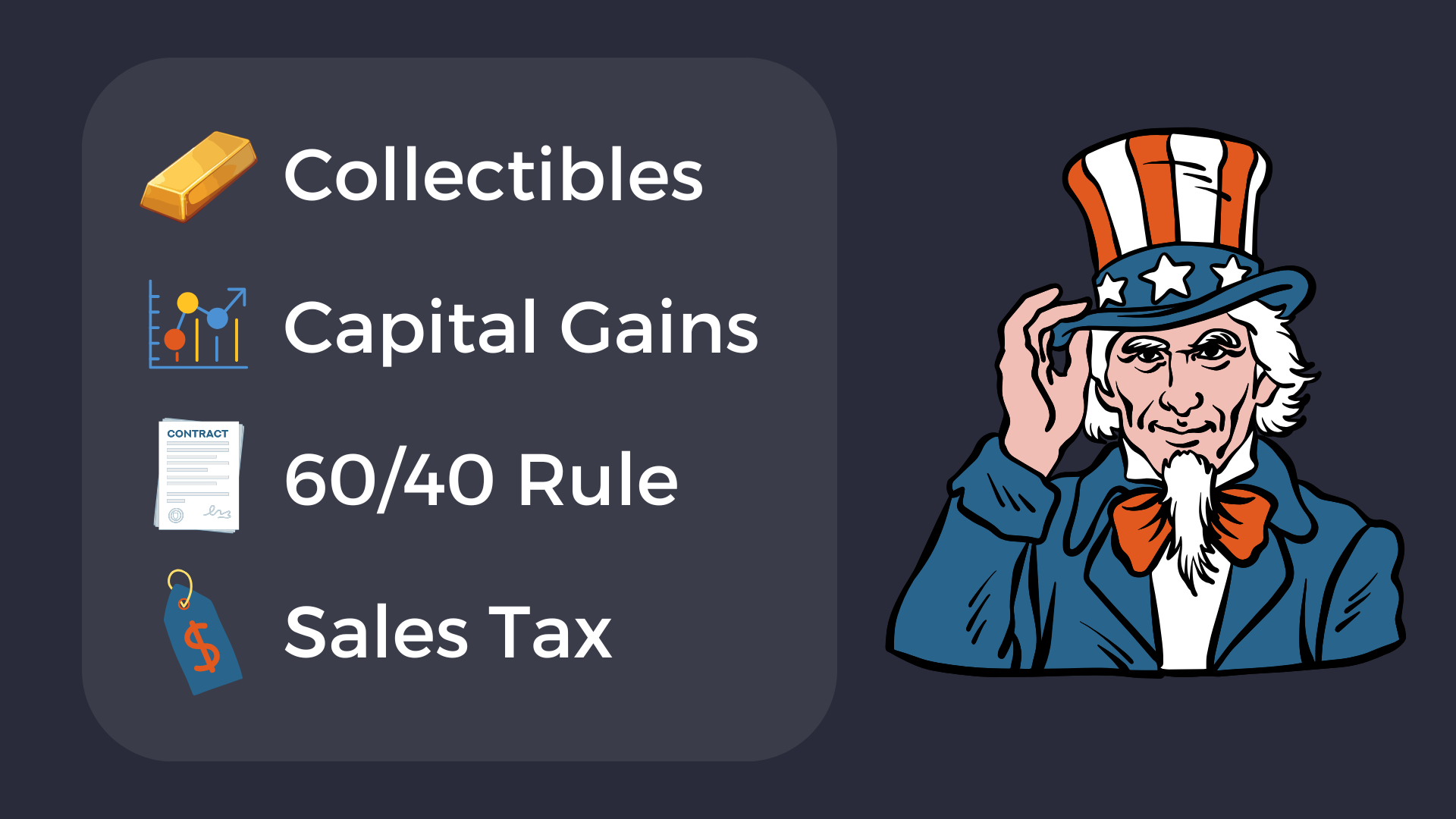

This article offers a comprehensive overview of U.S. state and federal tax rules for precious metals.

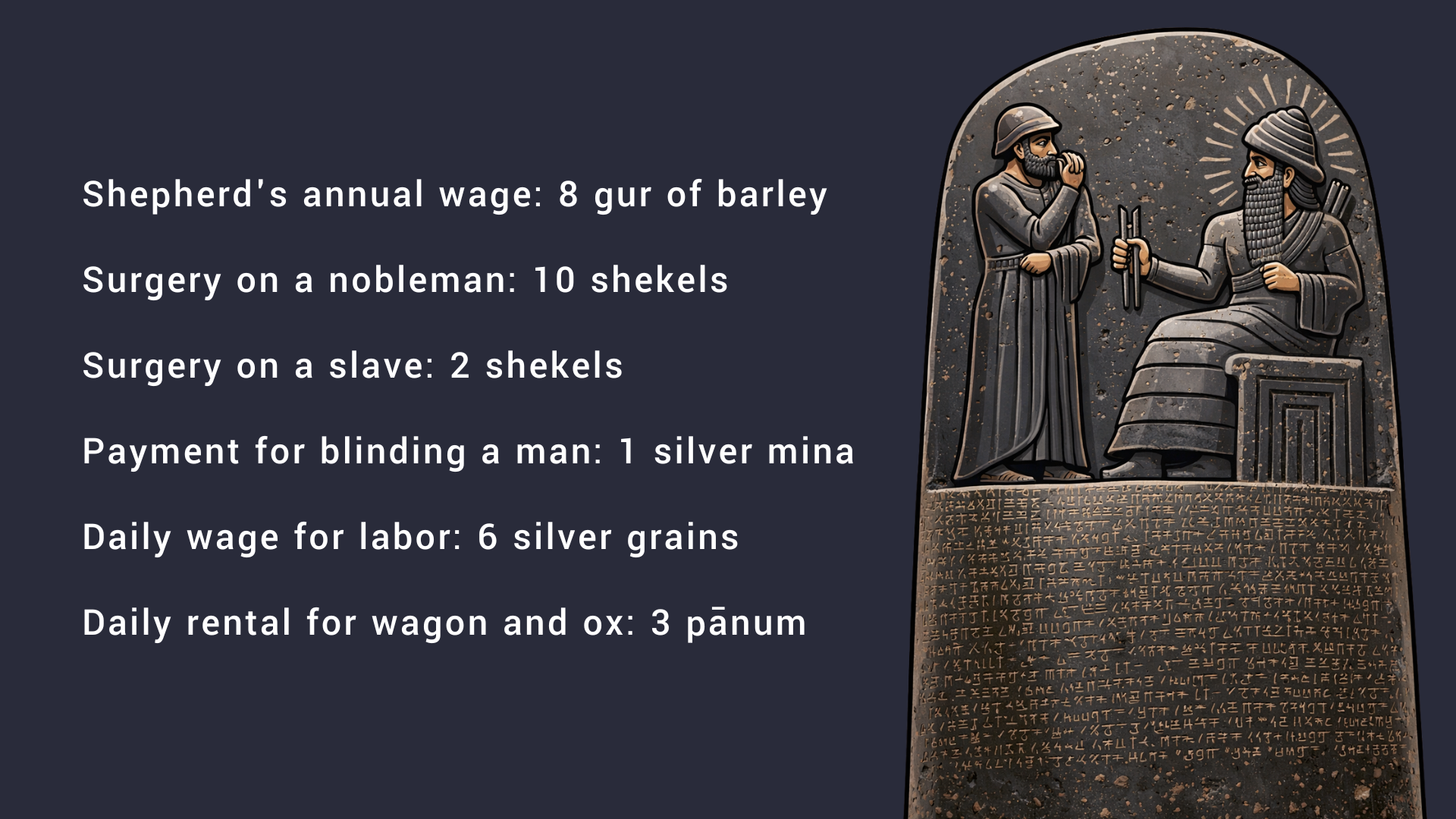

This article uses gold as a stable benchmark to translate wages and prices from Hammurabi’s Code into modern terms.

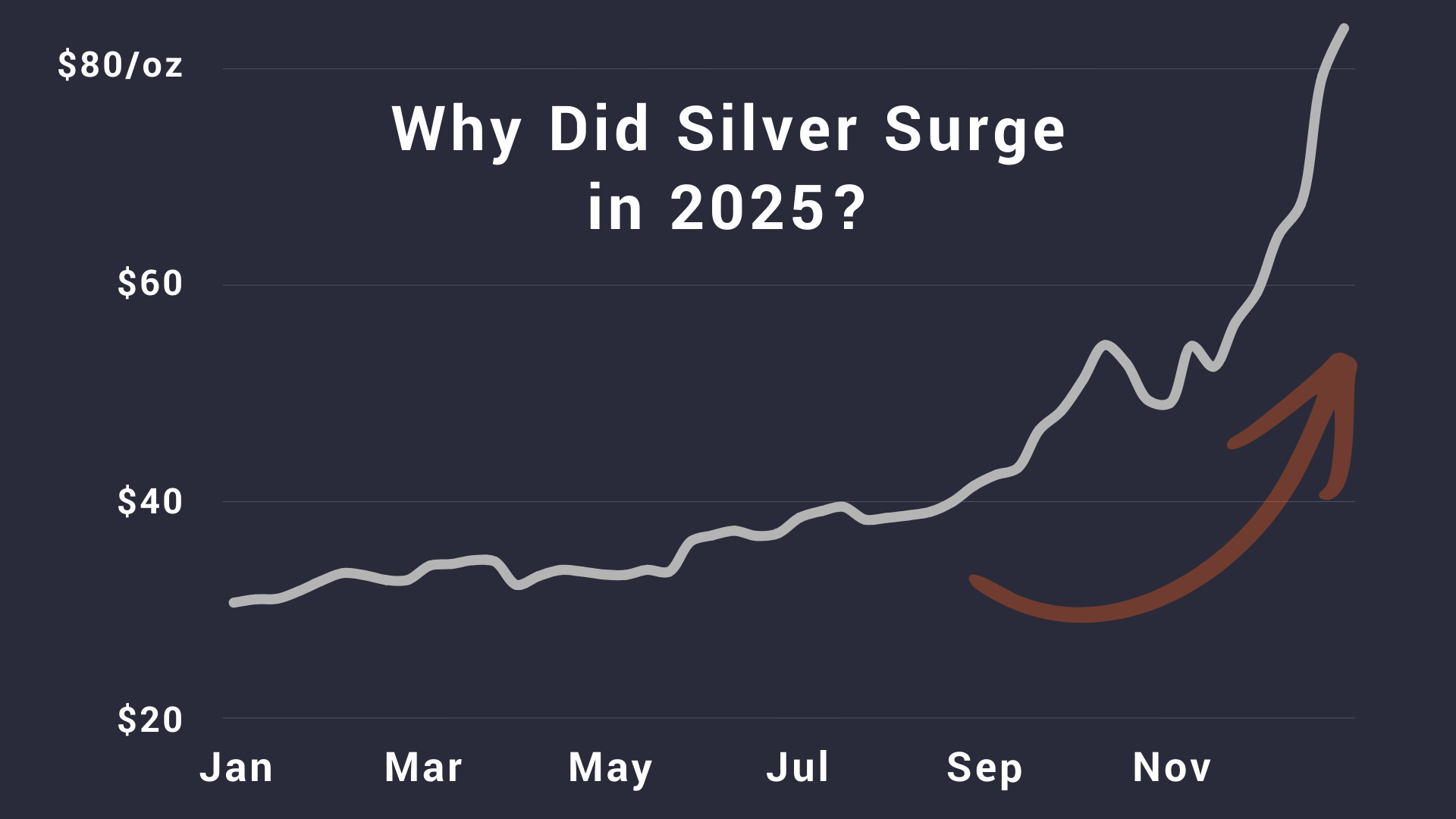

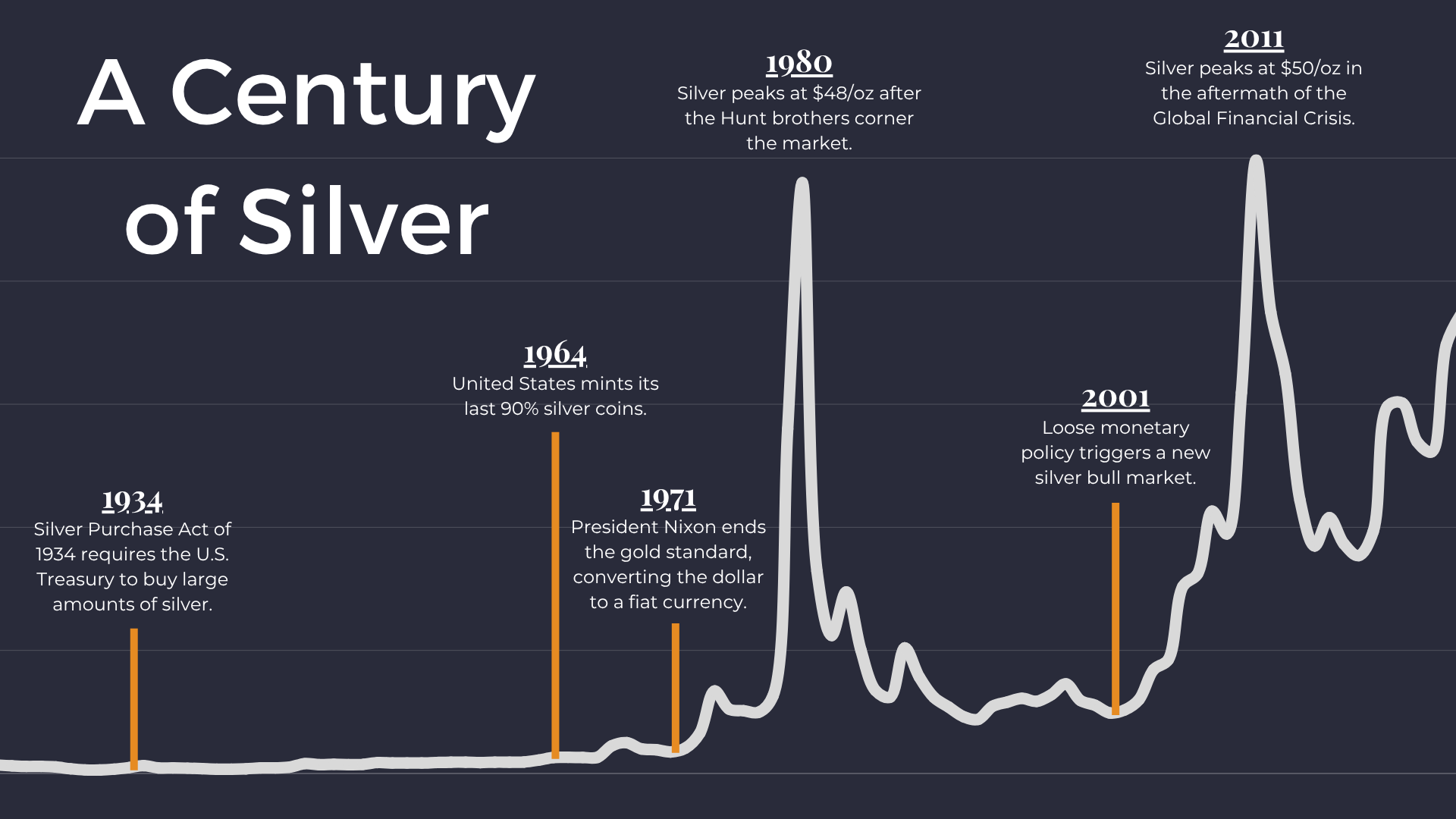

In 2025, silver experienced a radical repricing—from a low of $28.3/oz to a high of $87.7/oz (a 210% move). In this article, we will explain the forces that caused the silver surge.

Gold and oil are the two most important commodities in the world. Tracking the gold/oil ratio is like watching the tug-of-war between Wall Street and Main Street.

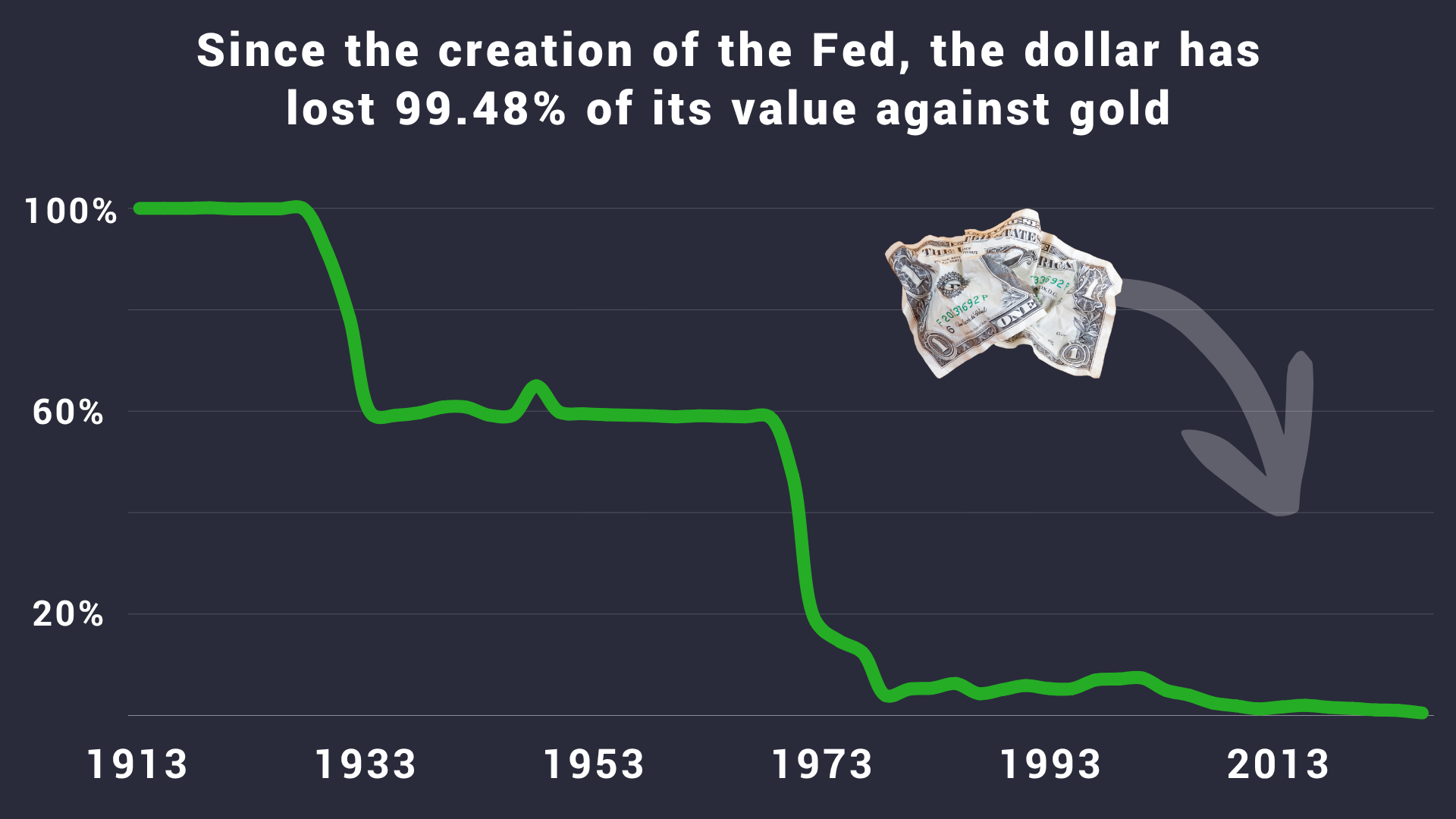

Gold and the US dollar were once inseparable partners. Now they are sworn rivals. Let's dig into the breakup that shaped the modern economic system.

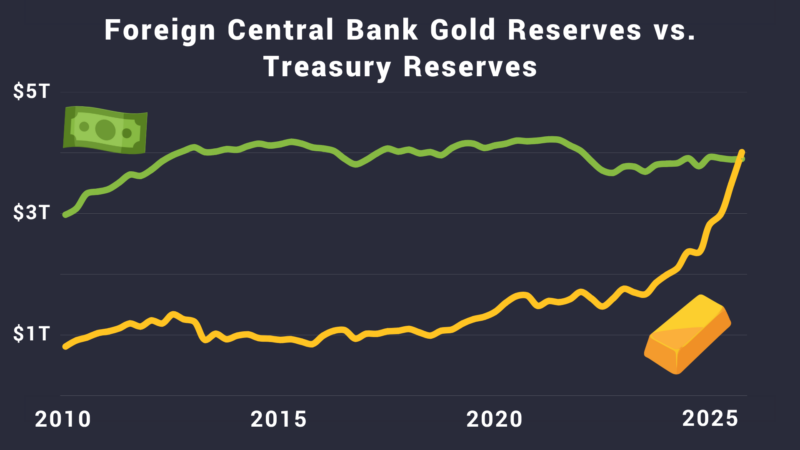

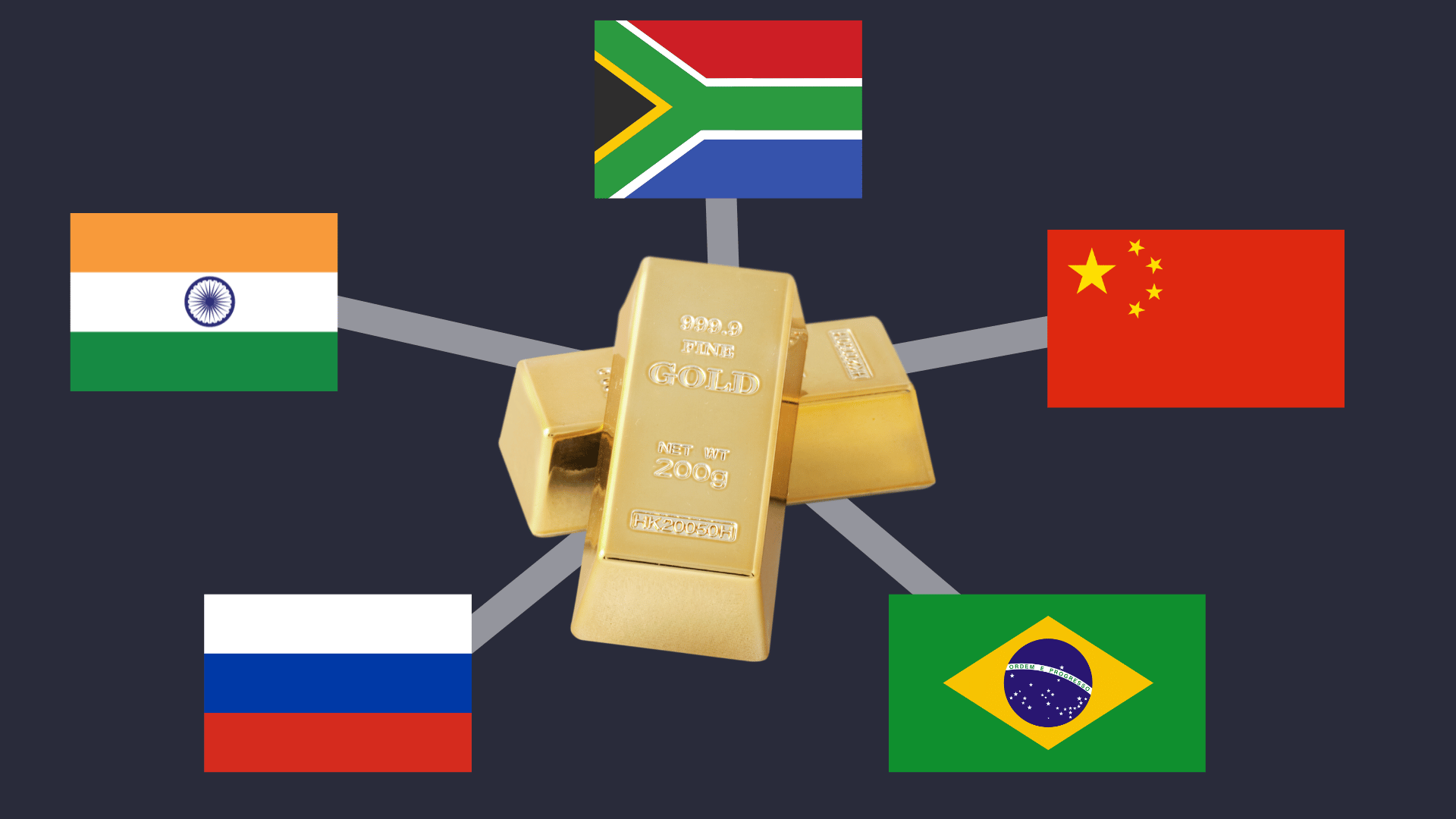

The value of central bank gold reserves just surpassed the value of foreign U.S. Treasury holdings. When the biggest players in the world swap bonds for bullion, it’s worth paying attention.

We’ll explore the silver price history from 1925 to today and zoom in on recent decades (30-year and 10-year price trends).

Silver is one of the most attractive investment opportunities today. Despite its growing applications in technology, silver remains extremely undervalued.

We’ll explore the gold price history from 1925 to today and zoom in on recent decades (30-year and 10-year price trends).

Trump’s tariffs have sent gold to an all-time high. Markets expect tariffs to cause some combination of higher inflation, a declining U.S. dollar, geopolitical tensions, and more foreign gold demand.

Discussions of a new “BRICS currency” are gaining widespread attention. This article explores why an increasing number of foreign nations are attempting to “de-dollarize,” and why gold has emerged as a viable alternative to the USD as the global reserve currency.

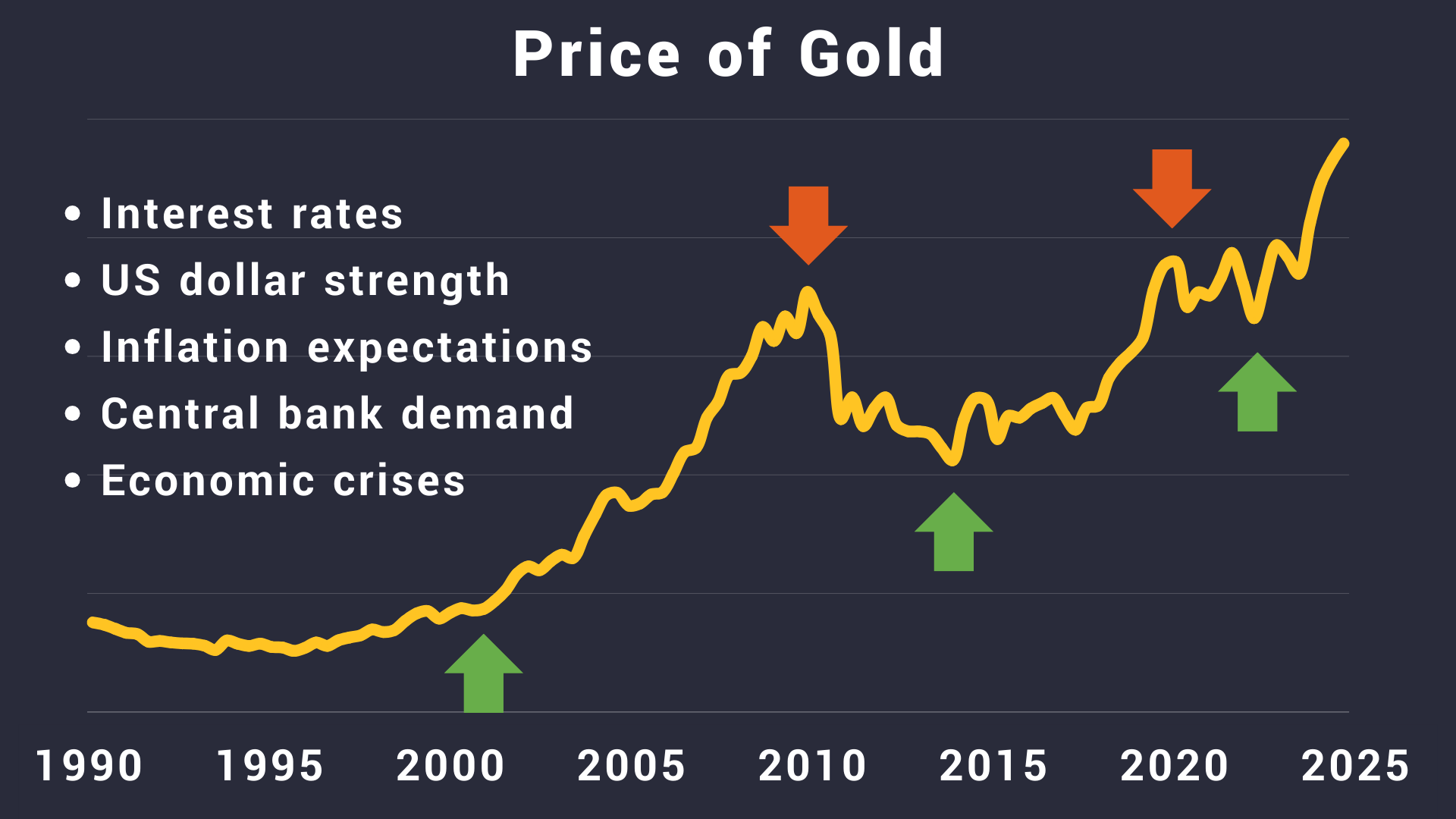

Gold and interest rates have an inverse relationship. When interest rates fall, the price of gold tends to rise, and vice versa.

The “gold spot price” refers to the price an investor will pay for the immediate delivery of one ounce of gold. But who decides it?

The price of gold rises when some event encourages marginal buyers to buy, or discourages marginal sellers from selling. This article discusses the top 10 factors that drive gold prices.